By super.AI

Artificial intelligence (AI) is disrupting critical business processes in virtually every industry, and finance consistently reports the highest levels of AI maturity out of them all. By leveraging new technology like AI, the financial services sector has made banking applications and products more user friendly and kept legacy institutions technologically relevant. However, this head start doesn’t mean there aren’t issues.

This article covers the challenges facing artificial intelligence in the financial services sector, including an overview of AI adoption, common obstacles and how to overcome them, as well as useful resources for taking advantage of artificial intelligence.

AI has been gaining prominence in the financial world since the 1980s, when expert systems were first used to predict market trends, provide customized plans, and reduce the risk of human mistakes. People working in the finance industry have been quick to recognize the potential of AI, and being early adopters has paid off. For example, hedge funds that leverage AI vastly outperform those that don’t. Research from consulting firm Cerulli found that “AI-led hedge funds produced cumulative returns of 34% [over the past three years]... compared with a 12% gain for the global hedge fund industry over the same period.”

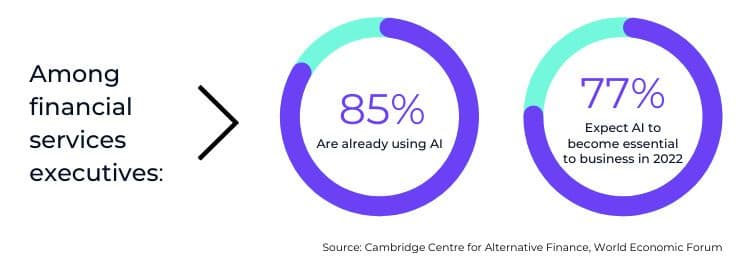

According to a 2020 World Economic Forum survey, 85% of financial institution executives are already using artificial intelligence, and 77% expect AI to become essential to their business in 2022. Separate research from O’Reilly Media found that people in the financial services sector have the highest levels of AI maturity when compared with other industries. Although AI adoption in financial services is far along in a relative sense, it still has a long way to go. Next we’ll cover some of the obstacles facing AI adoption in financial services.

Early adoption means the financial services industry already has a well defined list of industry-specific AI roadblocks. Data privacy and security, data silos, access to high-quality training data, satisfying regulatory requirements, and skills gaps are some of the most essential challenges for organizations to anticipate and prepare for in order to ensure forward momentum isn’t stalled due to unforeseen blockers.

Financial services providers must collect, process, and store huge amounts of sensitive data that requires robust security and protection protocols. Additionally, increasingly strict data privacy laws make it prudent for financial services organizations to be aware of existing and forthcoming regulations. When building AI solutions, financial services providers need to take the following into account:

Siloed pools of data are a massive blocker for artificial intelligence. Either due to regulations, company culture, or technology, businesses often find themselves with siloed units that can’t (or don’t want) to be brought together. Unfortunately, AI doesn’t like this.

As mentioned above, AI relies on massive datasets that must be readily available for processing and analysis. Additionally, because financial services organizations collect and generate huge amounts of data each day, customer data is often spread across a number of different systems with varying degrees of compatibility. This complexity, combined with an unclear or altogether missing data governance program, presents a major challenge to AI. Fortunately, there are solutions:

A surefire way to solve technology problems is to use more technology. Here are a few tech-driven solutions to overcoming data silos:

In order for financial services providers to build effective AI solutions, a clear strategy must be developed to ensure data is accessible to everyone that needs it. Process-driven solutions to data silos may involve technology, but are focused on democratizing access to data across organizations. This includes:

It can be difficult for companies to source high-quality data, especially unstructured data. Of course, large technology companies like Apple, Amazon, Facebook, and Google collect huge amounts of data every second of every day. But smaller companies aren’t so fortunate. A former commissioner at the Federal Trade Commission (FTC), Rohit Chopra, went so far as to say, “Vast troves of consumer data collected by big technology companies allow them to gain a competitive edge and pose a threat to competition by creating entry barriers.”

Some pundits have argued for a “progressive data sharing mandate” that would require organizations of a certain size to share anonymized data with smaller rivals. Beyond this, even if companies can get good unstructured data, structuring it so that it can be used effectively for AI-powered automation is its own distinct challenge. Both of these issues have solutions:

In computing a black box is a system that can be observed in terms of its inputs and outputs, without understanding how it works internally. The financial services industry is heavily regulated, and unexplainable AI software poses a unique hurdle for regulators as they want (and need) to understand how a given model works.

Explainable artificial intelligence (XAI) attempts to use methods and processes to ensure human users can trust and understand the results from machine learning algorithms. This emerging concept will only become more important as intelligent machines play an increasingly greater role in our lives, making it essential that we understand how they reach conclusions. For financial services providers considering building or implementing artificial intelligence must keep AI explainability top of mind.

There is also another class of problems that center around a lack of resources and skills to implement AI at scale. It’s often easy to create a small demo project that looks really nice, but to implement at scale is something else entirely. This issue is compounded by the rapid pace at which AI technology is advancing, making it difficult for people to upskill quickly enough. Fortunately, no-code and low-code AI make it possible for non-technical business users to participate in building artificial intelligence solutions.

For example, super.AI’s Unstructured Data Processing (UDP) Platform makes it possible for anyone to train, test, and deploy custom AI solutions–all without learning to code. As platforms like ours grow and evolve to solve an increasingly broader set of problems, they will become essential tools that non-technical workers interact with on a daily basis.

Despite all the challenges mentioned in this article, artificial intelligence is very much worth pursuing for financial services providers. From cost savings to productivity improvements, the benefits are huge. A few of the upsides to adopting of AI in financial services include:

At super.AI, our mission is to automate boring work so that people can be more human. We strive to make artificial intelligence available to everyone with both the technology we build and the resources we create. If you’re interested in getting started with AI in financial services, check out the following resources:

Most invoice problems aren't processing problems — they're capture problems. Learn what invoice data capture is, where it breaks down, and how AI fixes it.

Manual document processing costs more than most teams realize. Learn what document process automation is, how it works, and what to look for in a platform.